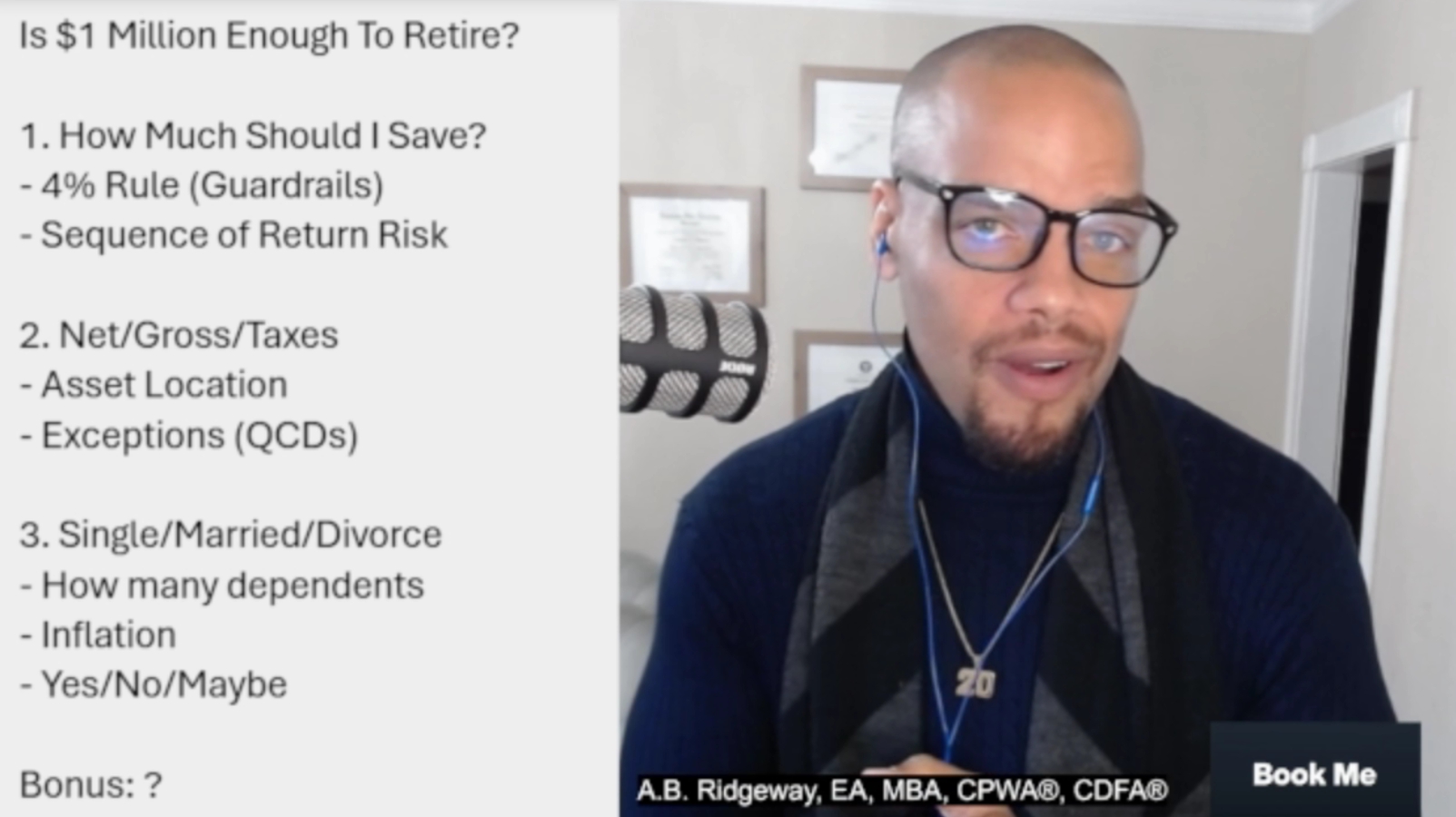

Is $1 million STILL enough to retire? | Financial Advisor Explains

The perception that $1 million ensures a comfortable retirement is outdated due to rising costs and increased longevity. Retirement planning should focus on individual lifestyle needs rather than an arbitrary figure. Factors like the 4% rule, taxes, asset location, and personal circumstances are critical to determining financial readiness for retirement.